News last week that some of Rolex’s top brass are taking senior roles at Bucherer could be viewed as little more than a technicality, with limited day-to-day impact on how either business is run.

Or, it could be seen as Rolex seizing control of Bucherer, opening the door to its watches effectively being sold directly to consumers through the 100-odd Bucherer (and Tourneau) showrooms around the world.

The difference between these two strategies is monumental, and could shape the next decade of luxury watch retail in Europe and the USA.

If Rolex chooses to favor Bucherer, allocations to independent jewelers and massive retail groups including Watches of Switzerland, The Hour Glass, and Ahmed Seddiqi & Sons could be impacted.

Rolex might also block business plans for these groups and family-owned independents to expand the real estate they devote to the brand through larger stores, refurbishments or new showrooms.

If Bucherer is competing in any city with these other Rolex ADs, it could get the green light to grow more easily that its rivals.

If a Rolex AD wants to retire or sell their business for any reason, Bucherer could get first refusal to buy it.

These are the types of changes that Rolex could pursue by stealth.

They would be slow, incremental, but potentially life-threatening for other Rolex partners squeezed out of opportunities.

They might find themselves paralyzed like a frog that boils to death because the temperature of water rises slowly around it and it fails to leap out.

So which way will Rolex go?

In the absence of any additional commentary since first announcing it was acquiring Bucherer, this time last year, we can only refer to statements made by Rolex at that time for guidance on how the two companies might alter course in the future.

Rolex’s corporate communications said in August last year that Bucherer’s management will remain unchanged, but the company will be integrated into the Rolex group operation once competition authorities have approved the takeover.

“This move reflects the Geneva-based brand’s desire to perpetuate the success of Bucherer and preserve the close partnership ties that have linked both companies since 1924,” the company said.

Nothing has happened since this statement from Rolex in August 2023 that contradicts it.

Competition authorities across Europe approved the takeover earlier in the summer, and the appointment of several leading Rolex executives to board level positions at Bucherer is covered under the stated plan to integrate the retailer into the Rolex group operation.

So far, so incremental, but with Rolex’s top team eying the books of Bucherer, they will get a perfect view of the P&L for a 100-door global retail group.

What might these figures reveal?

Bucherer and Rolex are private companies with no obligation to publish headquarters accounts so we will never know for sure.

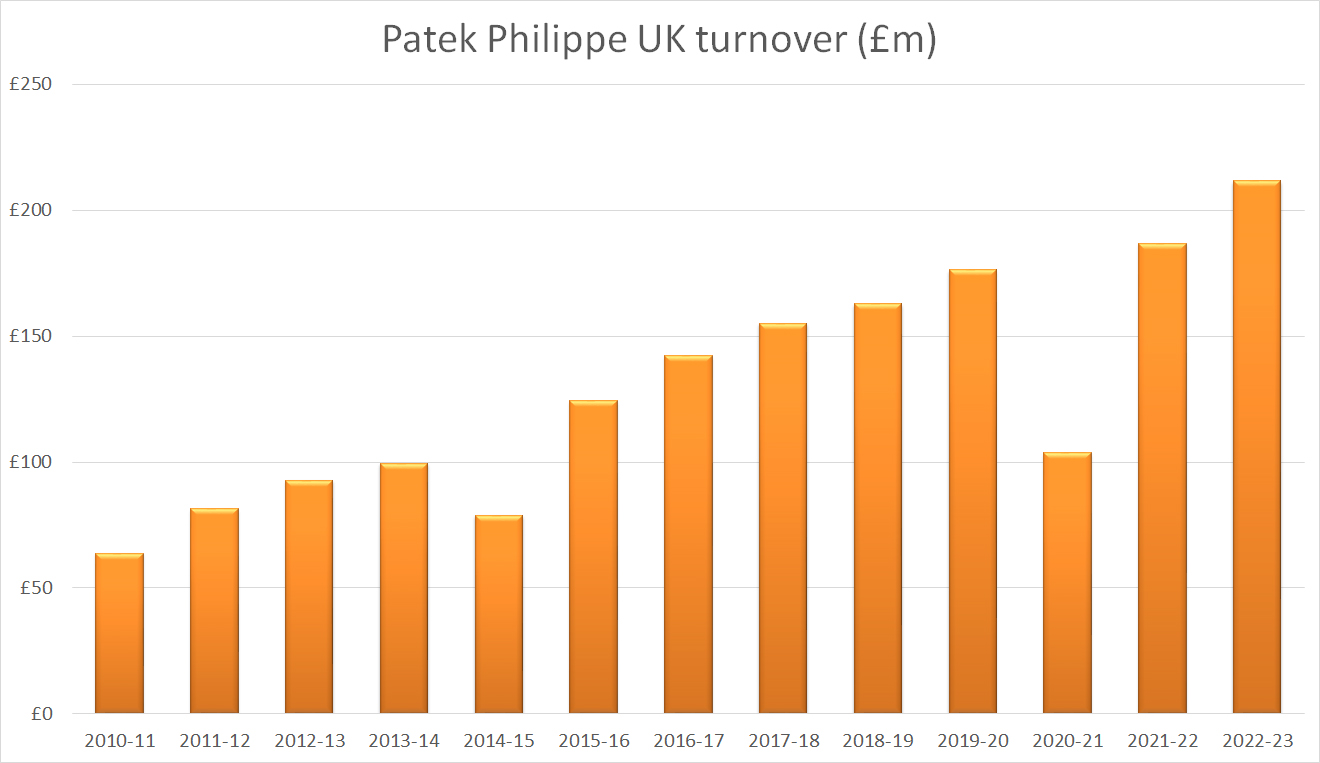

They both operate in the UK, where both their in-country operations are mandated to reveal their financial reports, so we could compare those results.

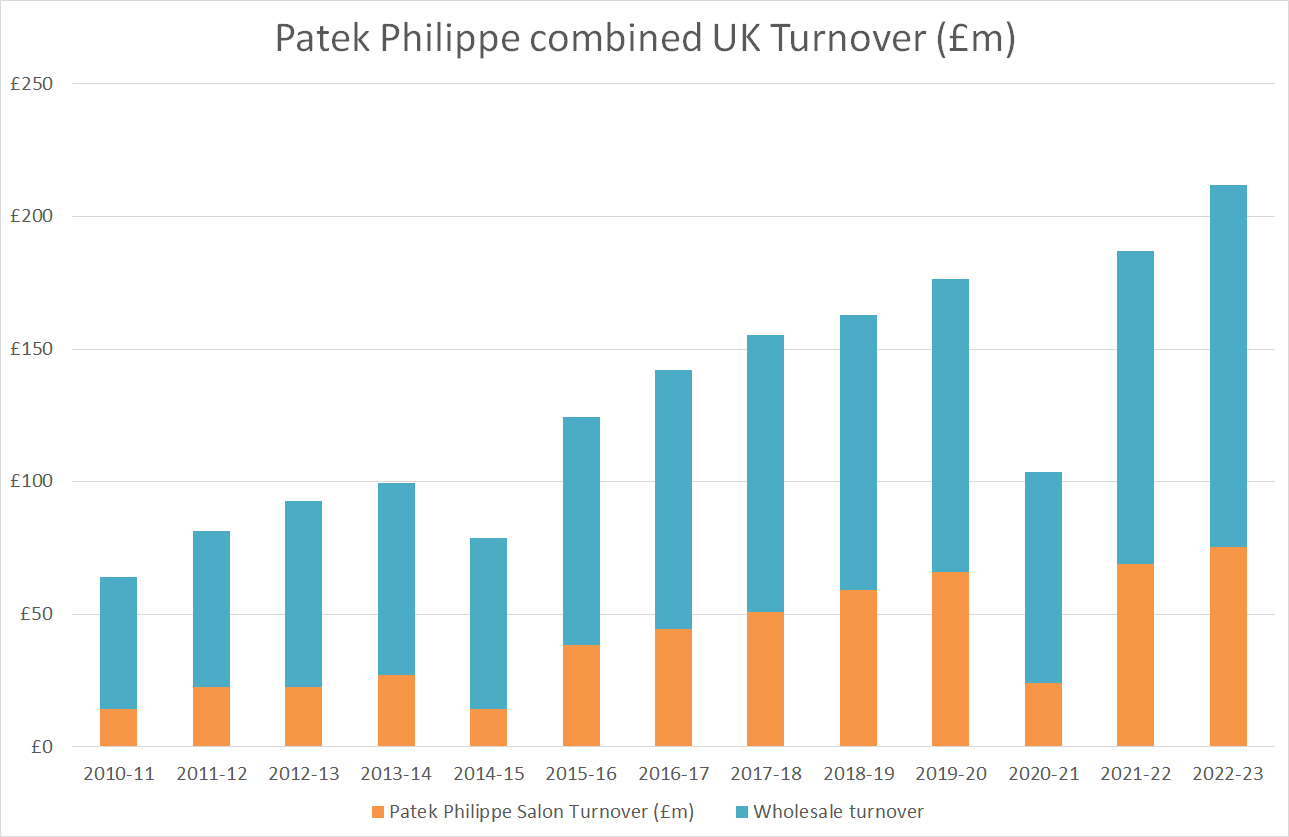

However, rather than measuring the performance of Rolex against Bucherer in the UK, I think it is far more interesting to look at another company in their field: Patek Philippe.

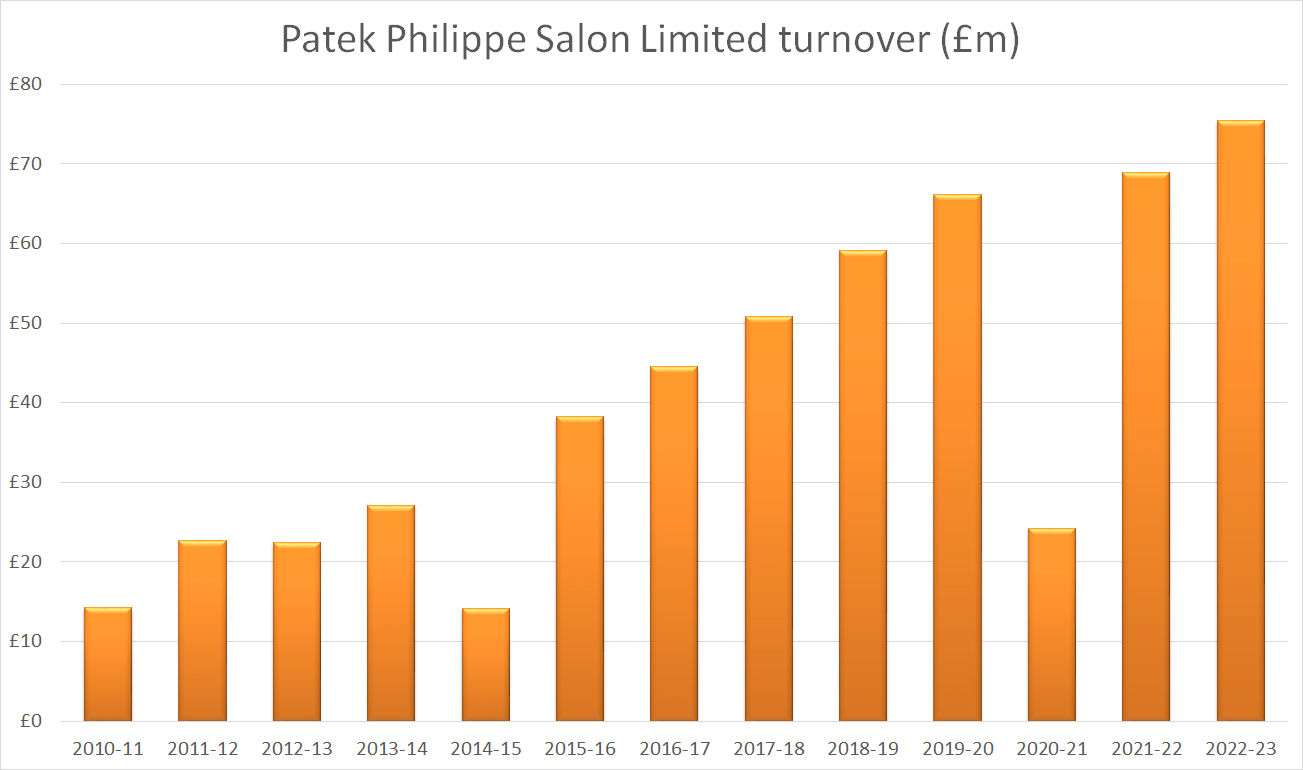

Why? Because Patek Philippe operates as both a wholesale business in the UK with a very similar business model to Rolex, and as a retailer with a directly owned and operated boutique on London’s Bond Street.

This boutique accounts for the cost of watches by showing them as transactions with the UK-based Patek Philippe wholesale operation.

By comparing the accounts of Patek Philippe the wholesaler with Patek Philippe the retailer, we can get an insight into the potential benefits of Rolex continuing to sell through its network of authorized dealers or selling direct.

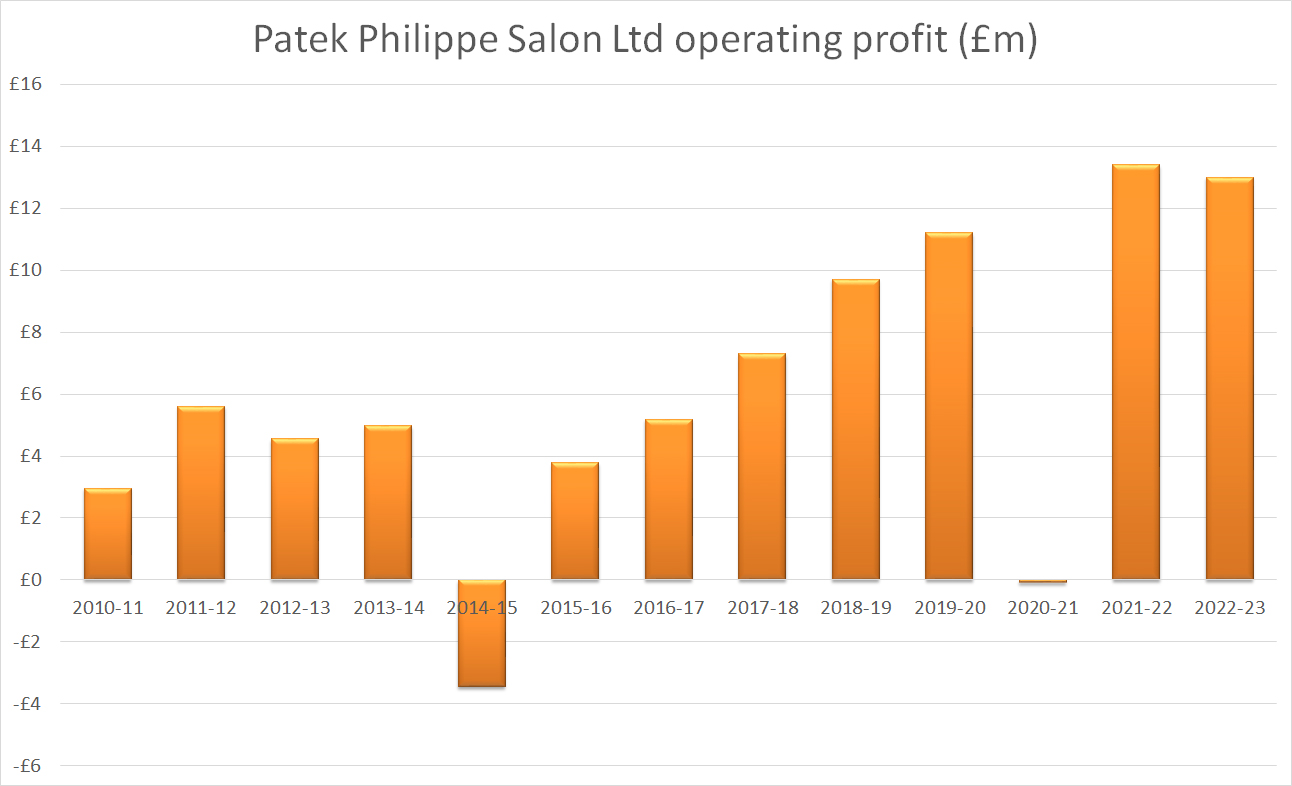

Patek Philippe Salon Limited, the company responsible for running the Bond Street boutique, generated revenue of £75 million from direct sales in its 2023 financial year, a gross profit of 35% (the same margin that an authorized dealer makes from buying and selling a Patek Philippe watch) and an operating profit of 17% after overheads are subtracted.

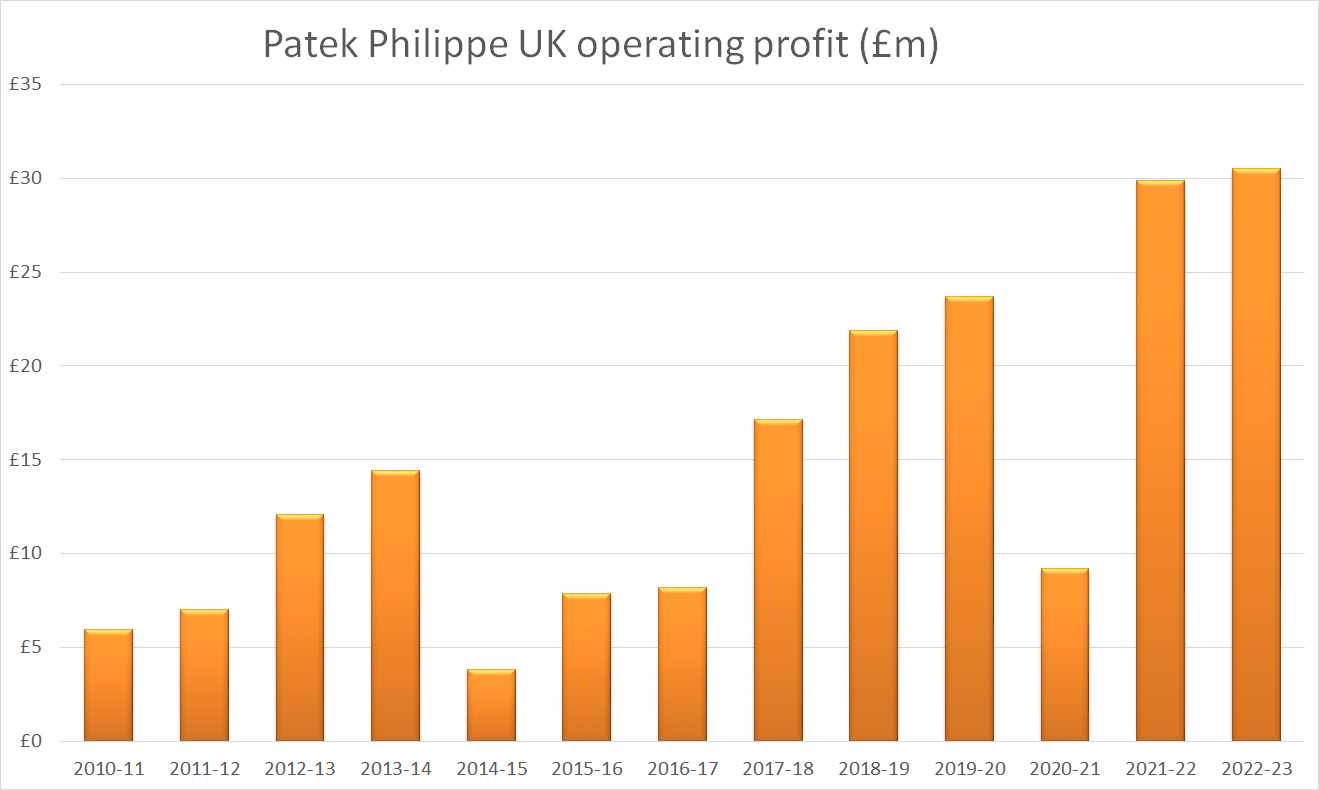

Rhone Products (UK) Limited, the trading name for all Patek Philippe operations, reported turnover of £211 million, gross profit of 24% and operating profit of 14%.

These figures include the contribution from Patek Philippe Salon, meaning that the profit margin for wholesale, in isolation, would be a little lower.

While Patek Philippe Salon does operate at higher margins, it is not the huge difference that some might assume.

This is important when we consider what Rolex might do next.

Even assuming, as we see from the Patek Philippe UK example, that margins are higher selling watches through an owned boutique, the difference is not so great that it would be a no-brainer for Rolex to follow suit by opening its own showrooms, or running a retail operation through Bucherer.

Much more likely, in my opinion, is that Rolex’s improving knowledge of how retail works pushes it to continuously insist on rising standards from its authorised dealer network.

From my conversations with these ADs over the past year, it is their view as well that their relationships with Rolex will endure, albeit with ever-ratcheting pressure to deliver exceptional experience to customers and, above all, maintain Rolex’s obvious market leadership in the prestige watch market.

Patek Philippe believes this is best-achieved by working with the very finest retail partners, and so does Rolex, not only because they are so successful within their own towns and cities, but also because they form a sort of hive mind that feeds intelligence up to The Crown.

Long may it continue.