Richemont doesn’t do wholesale for its Cartier and Van Cleef & Arpels jewelry, although it has opened franchise boutiques with these marques and their watches are widely distributed to authorized dealers.

According to Morgan Stanley’s 2023 annual report on the state of the Swiss watch industry, 40% of Cartier watches were sold through wholesale and 60% of Van Cleef & Arpel’s wrist-worn works of art went to partners.

It is a mixed picture for Richemont’s Specialist Watchmakers (SWM) brands. Only 40% of Vacheron Constantin’s output is sold through wholesale, for IWC and Jaeger-LeCoultre are at 55%, Panerai a little higher at 65%.

This includes sales into monobrand franchised showrooms like LV Luxury’s parade of linked Richemont boutiques in Las Vegas.

These wholesale percentages are below average for the industry. Rolex is 100% wholesale, Patek Philippe 85%; LVMH’s Hublot, TAG Heuer and Zenith are all over 70%, and it is a similar story for Swatch Group’s biggest brands, Omega (63%), Longines (90%) and Tissot (80%), Morgan Stanley, in conjunction with LuxeConsult, estimates.

Richemont’s direction of travel is to to either own or increase control over more of its global retail network.

Most visibly, this is seen in the mushrooming of branded boutiques, either internally run or franchised, and the rollout of its TimeVallée multibrand showrooms — again either owned and run by the group or operated by partners.

The latest opening is the first TimeVallée in the United States, run by the family-owned Kodak Group out of New Jersey.

TimeVallée aims to open beautiful multibrand showrooms in key locations, which gets Richemont closer to customers, even if a franchise partner is involved.

It has close to 50 stores around the world, more than half of which are in Mainland China. The network has been expanding eastwards in recent years, first across Asia and the Middle East, then into Europe.

Its first outpost in North America was in Montreal, Canada, before this summer’s opening as a franchise in New Jersey’s American Dream shopping mall where Watches of Switzerland also has a Rolex-anchored multibrand store.

TimeVallée around the world focuses predominately on selling watches and jewelry from Richemont’s maisons including A. Lange & Söhne, Baume & Mercier, Buccellati, Cartier, IWC, Jaeger-LeCoultre, Montblanc, Panerai, Piaget, Roger Dubuis, and Vacheron Constantin.

However, its stores also stock what might be considered rival brands including Bulgari, Carl. F. Bucherer, Chanel, Chaumet, Chopard, Corum, Franck Muller, Girard Perregaux, Glashütte Original, Gucci, Hermès, Hublot, Oris, Parmigiani, TAG Heuer, Titoni, and Zenith.

Richemont effectively has four retail plays: first, wholesale to its global network of authorised dealers running multibrand showrooms; secondly, its own internal boutiques; thirdly, monobrand boutiques run as franchises or joint ventures by retail partners; and fourthly TimeVallée showroom, run directly or with partners.

Oh, and the biggest branded stores of all are their global ecommerce sites, each of which sells more than any physical showroom on the planet, not least because they are fed a constant diet of highly desirable watches that are exclusive to these estores.

When you look at this mix, you can see there are still reasons for specialist retailers to work with Richemont and retain access to the hottest brands, particularly Cartier right now.

But the mood music around Richemont is not encouraging retailers to invest more.

Quite the opposite. Several retailers have told me, off the record, that they feel put-upon, even bullied to devote more space and better in-store positions to its brands, ideally opening monobrand boutiques.

If they refuse, they could lose the brands or find themselves competing with internal boutiques, rival franchise stores or a TimeVallée opening in their neighborhood.

Understandably, and entirely rationally, retailers are getting ahead of this tussle by devoting more of their time, money and real estate to brands that they trust to work with in long-term, potentially multi-generational, partnerships.

It is often reported that selling more directly to consumers is more profitable because a brand keeps more of the margin from every watch sold.

This ignores the cost of running retail with all its overheads, which show up in comparisons between the profit margins of brands that sell direct and those that favor wholesale.

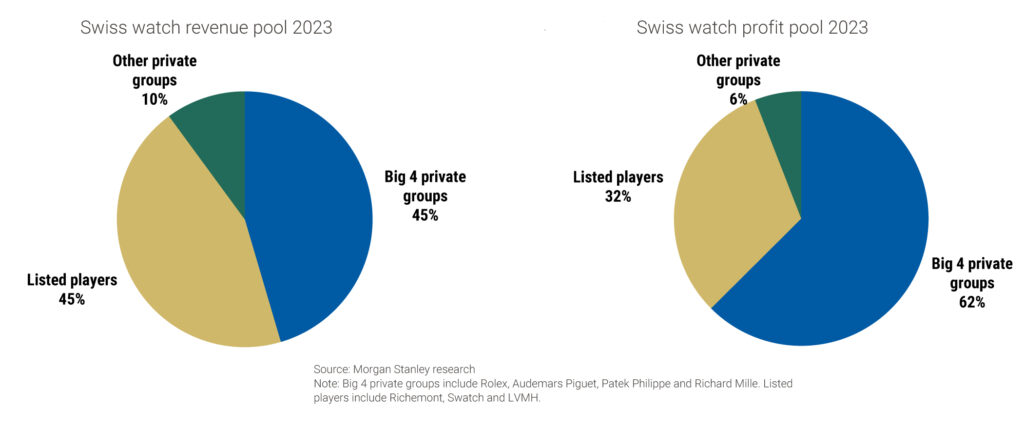

Morgan Stanley has an interesting pair of pie charts that suggest the assertion that DTC is more profitable is, at the very least, open to question.

Listed groups: Swatch, Richemont and LVMH, generated 45% of Swiss watch revenue last year but only 32% of profits.

The inverse is true for private groups: Rolex, Audemars Piguet, Patek Philippe and Richard Mille.

There are committed DTC brands on both sides including AP and Richard Mille among the privateers, so the picture is a little murky, but it calls into serious question whether selling direct is more profitable than wholesale, and this is during a record breaking year for Swiss watch exports.

This year’s more challenging market, in my view, favours specialist retailers much more than during a boom. They are simply more agile, more ingrained in their local markets, and more expert at the dark arts of generating irrational desire for the expensive trinkets they sell.

These more difficult conditions usually lead to brands leaning more heavily on their authorised dealers, and they should.

But Richemont may just find that, having mishandled these partners during the good times, they are not being welcomed with open arms now that times are tougher.