Earnings week for publicly-traded groups in the watch business is always a bit of damp squib because their results account for only a fraction of the entire market and are carefully crafted to give as little competitive information away as possible.

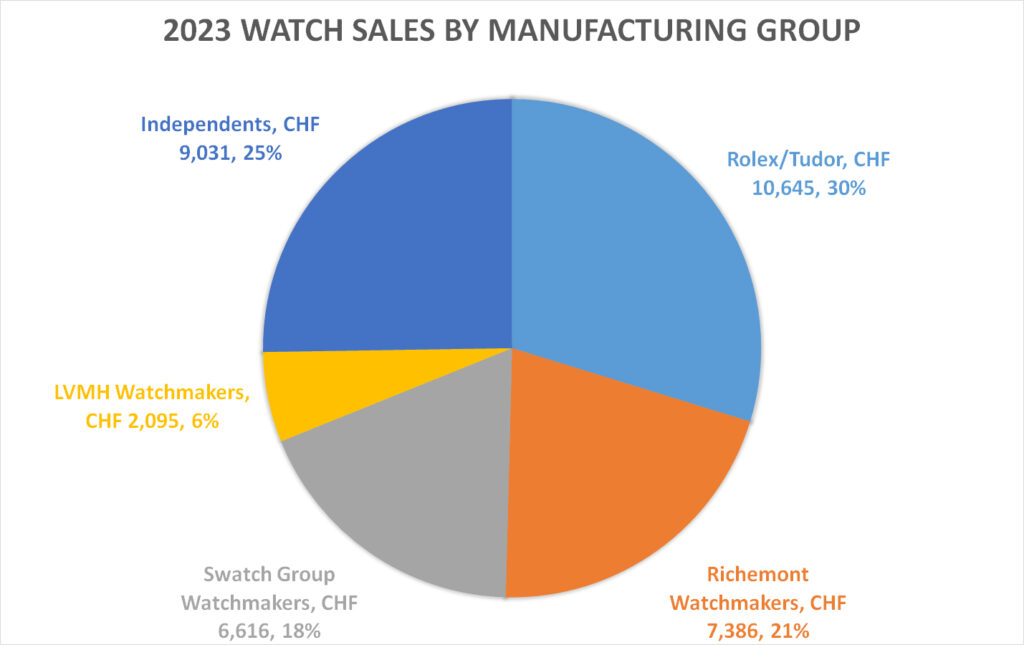

Taking Swiss watchmakers in isolation, which excludes the not insubstantial output of manufacturers in Japan, Germany and elsewhere, the market share of the groups totals 45%, according to Morgan Stanley estimates for 2023.

Rolex/Tudor, has 30% and independents, dominated by Richard Mille, Patek Philippe and Audemars Piguet, accounting for another 25%.

In the past week, we have heard the financial results for the latest quarter or first half of the year from LVMH, Richemont and Swatch Group, all of which have reported falling watch sales.

Swatch Group turnover dropped by 10.7% to CHF 3.4 billion in the first six months of 2024 as economic and political challenges in China, Hong Kong and Macau weighed on sales.

The fully verticalized group also suffered on the home front as weakening demand, coupled with a determination to maintain marketing programmes and keep its valuable manufacturing workers employed, squeezed operating margins.

Keeping its factories and workshops whirring was blamed for a drop in operating margin from 17.1% in 2023 to under 6% in H1.

A day after Swatch Group’s report, Richemont disclosed that sales for its Specialist Watchmakers, which excludes Cartier, dropped by 13% to €911 million.

LVMH’s Watches and Jewelry division, which includes TAG Heuer, Hublot and Zenith but is dominated by Tiffany & Co. and Bulgari, has reported a year-on-year drop of 3% in sales and a 19% decline in profit.

While it is clear that the past six months have been challenging for many prestigious Swiss watch brands, we do not have enough information to create a clear picture of what has actually gone on.

Every Rolex retailer I have spoken to in Europe and the United States has hinted that waiting lists are coming down, but business has never been better for the brand.

I am getting the same story for Patek Philippe and Audemars Piguet.

Richemont’s jewelry maisons division, home to Cartier and Van Cleef & Arpels, reported sales up by 4% YoY in its latest quarter, but doesn’t break down figures by brand or between watches and jewellery.

A bit of cross-referencing with Morgan Stanley’s 2023 sales estimates suggests Cartier watches accounts for around 20% of the Richemont jewellery maison’s total; Van Cleef & Arpels watches are under 10%. It is likely watch sales underperformed jewelry sales for these brands over the past six months, but we do not know for sure.

All of which suggests there is very little we can conclude about the broad sweep of the global luxury watch business from the results of the publicly-traded groups.

But here, for it is worth, is where I think we are:

The biggest brands with strongest demand since 2020 will have enjoyed rising sales in the first half of 2024. Waiting lists may be shortening, but they still exist for most watches from Rolex, Patek Philippe, Audemars Piguet and Richard Mille.

Watchmakers that are ostensibly known as jewellers — Cartier, Bulgari, Piaget and Van Cleef & Arpels — have held up better than those focused on selling predominately to affluent men.

The top end of the market has been less impacted by a cost of living squeeze in the West, so collectors’ brands like A. Lange & Sohne and Vacheron Constantin have held up better than the next price tier, for example Panerai, Hublot, IWC, Breitling and Omega.

I expect to see Breitling outperform its close rivals this year in terms of sales, but its profitability may be dented because it is carrying the cost of running so many boutiques.

TAG Heuer is benefiting from better brand recognition, particularly with its extensive network of boutiques, but sales are suffering and Tudor is gaining market share.