Secondary market watch price trackers including the Subdial Bloomberg index and Chronopulse by Chrono24 are showing prices bottoming-out in October last year and bumping along the bottom or rising slightly in the three months since.

WatchCharts/Morgan Stanley’s most recent Watch Market Report covering the fourth quarter of last year, tells a slightly different story with prices continuing to fall, by 1.5% over the prior quarter and by 1.2% over the same period in 2023 across the most traded watches globally.

Richemont’s brands were the worst performers, according to the report, with prices down by an average of 2.4% in the quarter.

Its average has generally been bolstered by the recent strength of Cartier, but even this jewel in the Richemont crown had a weak end to the year with prices dropping quarter-on-quarter by 2.2%.

Vacheron Constantin, Jaeger-LeCoultre, A. Lange & Sohne, and Piaget have all seen prices soften by over 2% since the summer of 2024.

LVMH’s stable of brands outperformed rival groups with an average quarter-on-quarter price drop of just 0.6%.

Zenith is the group’s smallest brand, but its second hand watches rose in price by an average of 0.6%.

This comparatively strong end to the 2024 took the chill of a difficult year where average pre-owned Zenith prices dropped by an average of 5.1%.

Moonswatch prices

At Swatch Group, prices across the portfolio dropped by 1.5% between Q3 and Q4. Its biggest brand Omega was roughly in line with a price drop of 1.3%.

Fading hype around the Swatch x Omega Moonswatch contributed to an 8.4% drop in secondary market prices for Swatch in the quarter.

Rolex prices

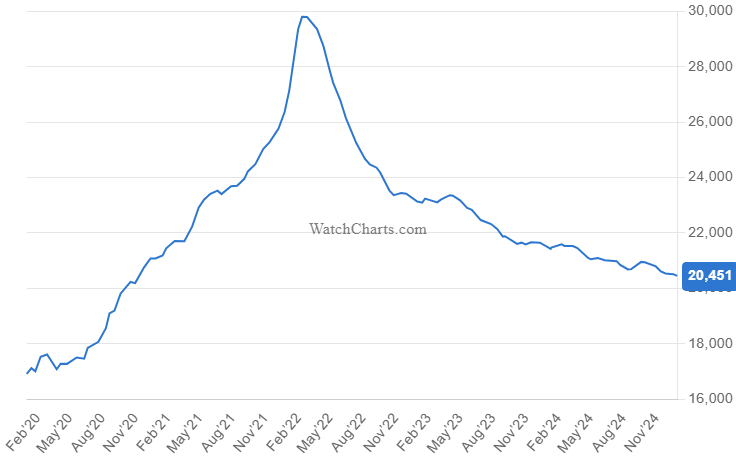

Rolex accounts for more than all other watch brands’ sales combined on the secondary market, and is responsible for price trackers, which are heavily weighted towards Rolex’s most traded professional watches, continuing to slide.

According to Watchcharts/Morgan Stanley, Rolex prices are now at four year lows; not only are its watches trading well-below peak prices in the spring of 2022, they are 3% below levels last seen in January 2021.

In contrast, Patek Philippe prices are still up by 28% since the beginning of 2021 and Patek Philippe average prices are up by 22%.

Vital to the enduring demand for pre-owned watches from the big three is that most of their models still trade at above retail prices.

However, this claim is coming under pressure after 11 consecutive quarters of price declines.

For Rolex, 56% of models selling on the secondary market in January 2025 were trading for over their authorised dealer retail prices, which compares to 68% a year ago.

63% of AP’s watches trade at over retail today, a slight drop from 65% in January last year.

Patek Philippe has seen a similar correction. A year ago 45% of its references were trading at above retail prices. Now the proportion is down to 38%.

Rolex and Tudor both increased prices for new watches in January, which has closed the gap to the brands’ watches trading at over retail.

Analysts commentating on the Watchcharts / Morgan Stanley report say they expect secondary market prices to continue falling this year and the gap between primary and secondary market prices to increase.

“Most brands will need to navigate the widening gap between retail and secondary prices, driving more value-oriented consumers towards the secondary market and challenging brand perception by potentially making retail prices appear overpriced to some customers,” the report warns.