The current UK Labour government won last year’s election on the promise of a ten-year programme of stability and renewal for the country.

With a stonking majority, it was hoped some tough choices could be made early in the current parliament that would deliver a predictable path to sunny uplands just in time for the next election.

The problem with ten- or even five-year plans is that they tend to fall apart on first contact with reality, not least because they are overly based on past performance being extrapolated far into an uncertain future.

This is not surprising since nobody has 20-20 vision over what will happen in the future, but it is a crude exercise of questionable benefit, particularly outside of authoritarian states like China.

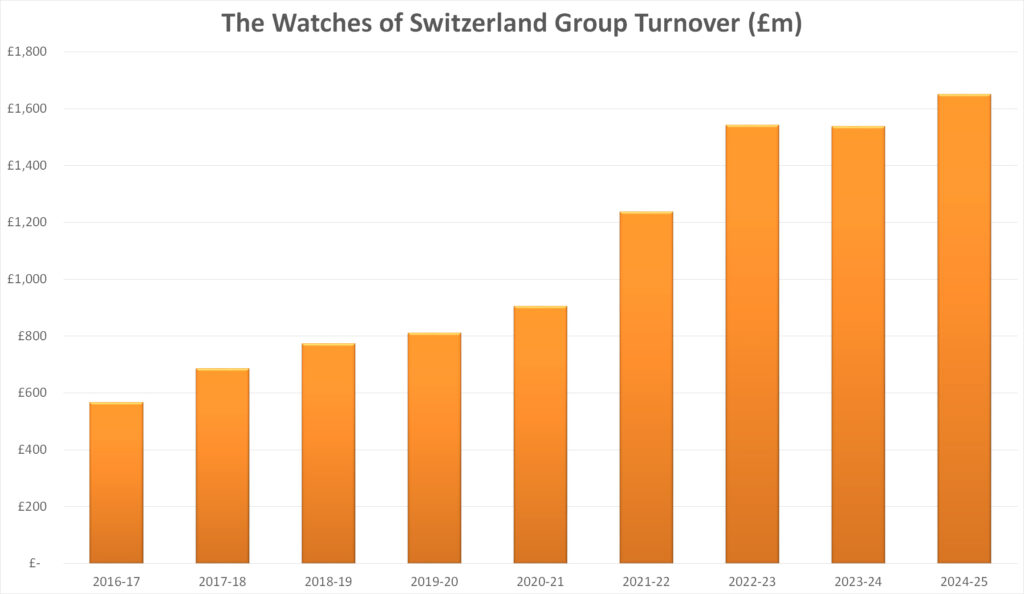

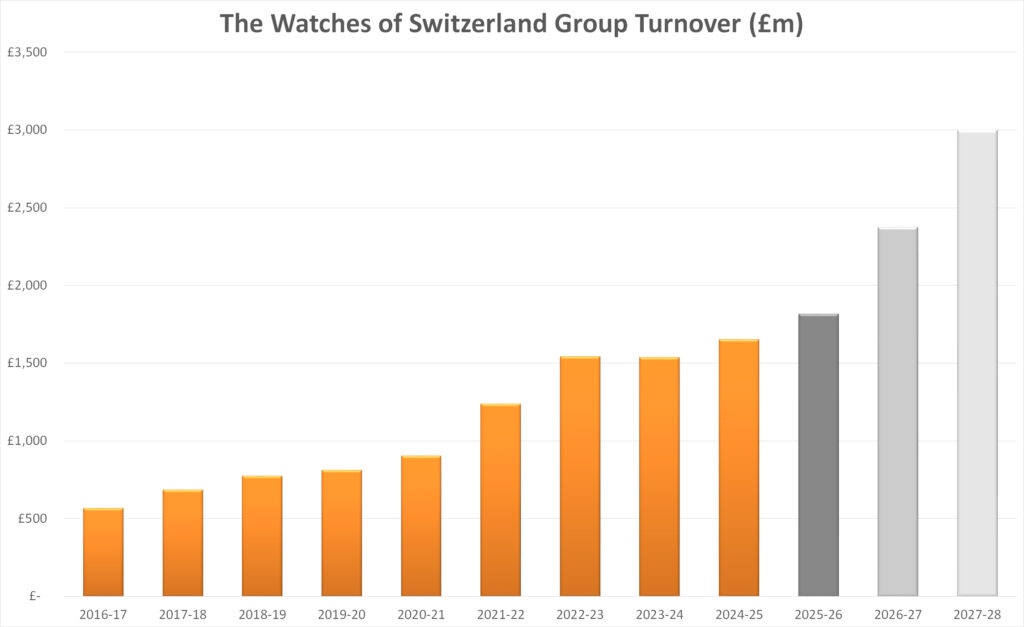

I was therefore surprised back in 2023 when Watches of Switzerland Group went public on what it dubbed its Long Range Plan, which describes a path to double revenue from its FY23 base of £1.54 billion to exceed £3bn by the end of FY28.

An awful lot would need to go right to add £1.5 billion in sales over five years, which required average annual growth of over 14%.

There were reasons to believe, back in 2023 when the LRP was unveiled, that the required growth was not especially bullish.

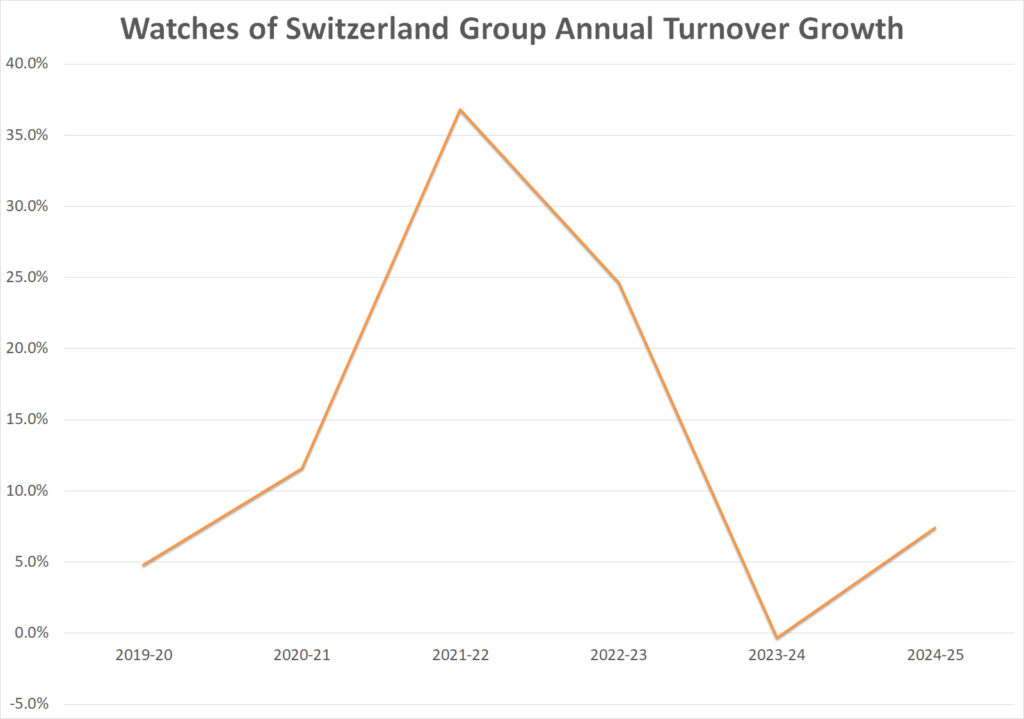

Even in the peak pandemic period, the group’s FY21, it grew by over 11%. It followed this with eye-watering growth of 36.8% in FY22 and 24.6% in FY23.

It is worth reflecting on how confident WoSG was feeling as it drew up its LRP in 2023.

“The Group is stronger than it has ever been, and we are tracking well ahead of the original plan we outlined in 2021, with a diverse pipeline of projects already scheduled for FY24, FY25 and FY26, which includes our strongest ever pipeline of committed Rolex projects. Our longstanding brand partnerships, leading multichannel capabilities, sophisticated marketing, and exceptional client service elevating the luxury experience truly sets us apart,” the group’s chief executive Brian Duffy said at the launch of the LRP.

WoSG’s share price was £5.30 that week, already 70% down from its £14.70 peak at the end of 2021, but nobody thought the peak price was anything more than a get-rich-quick proxy bet on Rolex at the height of the flipper-driven bubble in demand.

Investors appeared to like the LRP because the price had risen from around £5 to over £7 between October and December 2023.

The problem for both the timing and the forecasts in the LRP was that WoSG thought recent history would make future annual growth of 14% a challenging but realistic target.

This was based on the assumption that its business model, which had delivered incredible growth since 2020, would keep delivering in the future.

That business model is beautifully simple: spend big on market-leading showrooms in the right locations and you will be doubly rewarded: first by brands — most importantly, in fact critically, Rolex — and secondly by clients who are prepared to sit on Rolex waiting lists while building a customer loyalty profile by continuously shopping at a Goldsmiths, Mappin & Webb, Mayors or Watches of Switzerland.

Both these presumptions came under strain almost immediately.

Just two months after WoSG launched its Long Range Plan in the November of 2023, it issued a profit warning in January 2024 that wiped 30% off its share price.

Notably, that profit warning was partly explained by the group receiving more steel watches from Rolex than anticipated and less in the much more lucrative gold.

Investors immediately started questioning whether Bucherer, which had been bought by Rolex in August 2023, was being favored with better allocations than its biggest rival.

I do not think that was or is the case. Rolex was simply making more steel watches in an effort to close the gap between supply and demand for its most popular professional pieces. Every retailer I spoke to at the time was reporting the same thing.

But that adjustment in supply from Rolex was not anticipated in the Watches of Switzerland Group Long Range Plan.

Nor were the difficulties of expanding into new markets through a combination of store upgrades, store openings and acquisitions.

The LTP anticipated expansion into mainland Europe that would contribute 4-6% of group sales at the end of the five years in FY28.

That plan has entirely failed. Not only were there no Western European retailers willing to be sold to WoSG, a handful of branded boutiques that opened, mostly in Scandinavia, have been closed or handed over to the brands.

All of Mr Bolton’s energy has now been refocused on the UK market where there have been acquisitions of showrooms from other groups, mostly Ernest Jones, and a relentless programme of upgrades across Goldsmiths, Mappin & Webb and Watches of Switzerland locations.

However, there have also been many store closures, evening-out to deliver anaemic growth on the UK side of the Atlantic since 2023.

It will be interesting to see how a new AP House, opened as a joint venture in Manchester earlier this year, and the ribbon-cutting on an iconic Rolex flagship showroom on London’s Bond Street will contribute in FY26, which we are in now.

The AP House opening is particularly significant because growth with AP may be needed to compensate for a likely lack of growth with Patek Philippe.

During a streamlining of its global network in 2023, Watches of Switzerland lost the brand in Manchester and from its Mappin & Webb boutique on London’s Regent Street.

Mergers & Acquisitions

A series of successful acquisitions prior to the 2023 LRP may also have been false prophets of future opportunities.

WoSG bought its stake in the high-growth American market with the acquisition of 17 Mayors showrooms in Florida and Georgia in 2017.

It cemented its position with the opening of several prestigious Watches of Switzerland showrooms in New York and Las Vegas, and broke new markets with the 2021 acquisitions of Betteridge in Greenwich, Connecticut, Timeless Luxury in Plano, Texas, and one of Ben Bridge’s boutiques in Mall of America outside Minneapolis.

It had also bought Analog/Shift in 2020, a respected specialist in pre-owned and vintage watches in the United States.

Since these deals, there has only been one significant acquisition in the form of WoSG buying the American distribution business of Roberto Coin.

That is a sign of the group’s growing interest in fine jewelry (it is opening a jewelry-only Mappin & Webb flagship in Manchester this summer), as part of a broader mission to reduce its dependency on a handful of watch brands dominated by Rolex, which is still thought to account for almost half of annual sales.

While the market has undoubtedly become tougher since the 2023 LTP, there have also been some tailwinds, most impactfully in the advent of Rolex’s CPO programme, which Mr Duffy now says is the group’s second biggest brand after Rolex itself.

Expertise gleaned through the acquisition of Analog/Shift has also fuelled an expansion of its non-Rolex CPO business.

The American market, where the group was reporting annual growth of 40% in the years leading up to 2023, has continued to power ahead of every other global market.

Effectively, what global share China and Hong Kong have lost over the past five years, the United States has gained.

Year-on-year, WoSG sales rose by 16%, Stateside, in FY25, while growth in the UK and Europe was just 2% (well below the rate at which prices have been rising for luxury watches).

The path to £3 billion

The question now is whether WoSG can get back on track to hit its LTP target of £3 billion in sales by FY28.

It is a tall order, but not impossible.

Annual growth in the first two years of the plan was well below the required 14%. Sales dipped by 0.3% in FY24 and rose by 7.4% last year.

The most recent year is encouraging, but to hit its £3 billion target in FY28, WoSG will have to grow by 22% over the next three financial years.

It is actually going to be tougher than that. In commentary alongside its FY25 financial results, the group provides a forecast for FY26 predicting growth of 6-10%.

Let’s assume the higher end of that spread: 10% growth would take turnover to £1.8 billion this financial year, which would leave the group requiring around 30% growth for each of the final two years of its LTP.

Organic growth, particularly in CPO and Rolex CPO, might add 10% per year, which would leave the Group £800 million shy of its 2028 target.

The group is primed and ready for acquisitions with around £95 million available as cash and cash equivalents, according to CompaniesMarketCap.com.

Should the right acquisition target come along, like buying another major multiple in the United States, I would expect this to be leveraged-up to whatever is necessary.

And, finally, there are known unknowns. Could Omega get its act together and become a true challenger to Rolex again? Can Cartier continue to gain momentum? Would jewellers like Cartier and Bulgari allow their jewelry to be sold alongside watches? How big can Tudor get? Will TAG Heuer and Breitling return to previous growth trends?

There is an awful lot to play for and I am sure this is the focus for Watches of Switzerland Group today rather than an arbitrary target set for 2028.

However, I cannot resist keeping an eye on that Long Range Plan because, if there is one thing I have learned from watching Watches of Switzerland over the past decade, it is an exceptionally well-run business with the potential to surprise and delight not only its clients, but also its investors.